Sri Lanka forex inflows US$2.3bn in September, imports surge to $2.0bn – Corrected

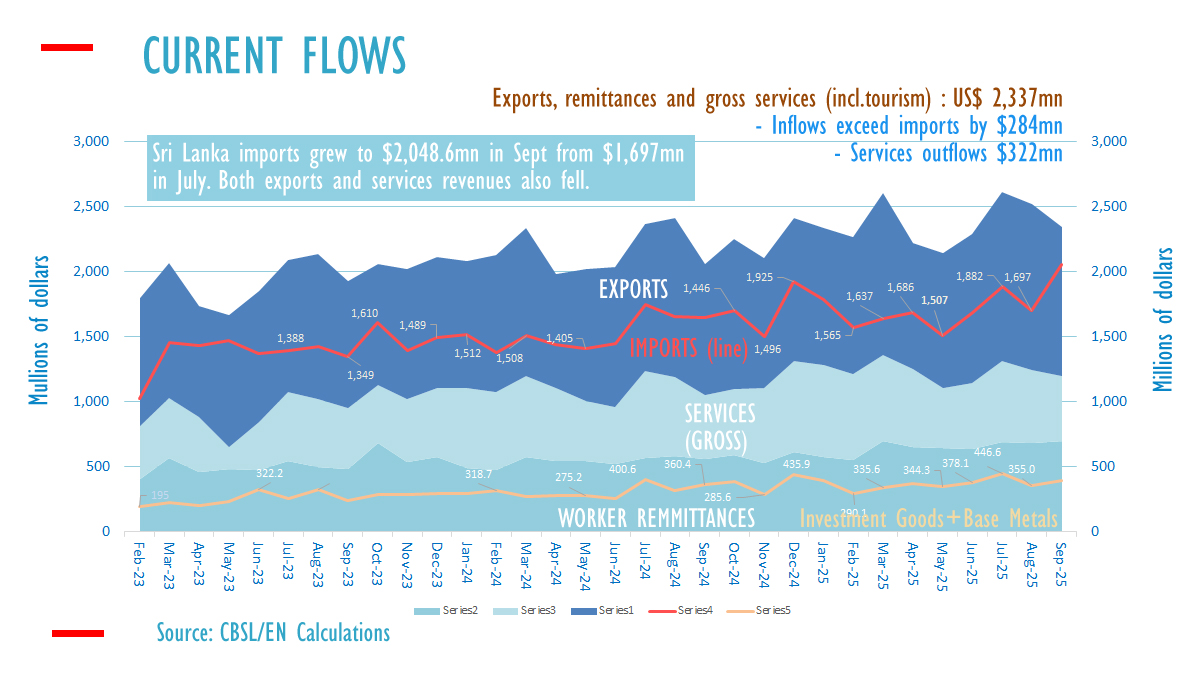

Sri Lanka’s current foreign exchange inflows were 2,337 million US dollars in September, down from 2,521 million dollars in August, while imports surged over 300 million dollars to 2,048 million US dollars, official data showed.

Gross current inflows exceeded merchandise imports by only 289 million US dollars in September down from around 600 million US dollars consistently over the past year.

Personal vehicle imports were 227.5 million dollars in September up from 198.9 million US dollars in August.

In September fuel imports were 440 million US dollars in September up from 255 million US dollars a month earlier, with an intermittent rise in crude oil and also an increase in refined products.

In general merchandise imports have tended to move in line with foreign exchange inflows up to September as the ability to import comes with earnings.

The only way a person or company can import any goods without current rupee earnings is to get credit.

Credit for one import such as cars have to crowd out other credit unless the central bank injects money though inflationary open market operations to allow banks to give loans t without deposits.

However inflationary open market operations have been paused for several months and there is now a scarce reserve regime and an active interbank market which crowds out each other and keeps the system in balance.

However, the central bank can still inject money through buy-sell swaps and give banks new money to make loans for cars or other imports which are out of line with external inflows.

Concerns have also been raised about a fiscal ‘buffer’ given past experience on how a ‘buffer strategy’ contributed to a currency crisis amid rate cuts in the 2015/2016 amid surging domestic credit.

Any money deposited by state banks in the central bank from the proceeds of the fiscal buffer, tends to be distributed to other banks when maturing bonds or bills are not rolled over and repaid with SDF funds.

Analysts have warned that any internally invested fiscal buffers cannot keep rates down and any rate reduction from fiscal buffers in the SDF window will lead to reserve erosion or currency depreciation unless the liquidity is redeemed with interventions.

The CPC in the past has taken suppliers credit to import fuel, and triggered ‘current account deficits’ especially when forex shortages emerged from inflationary open market operations deployed for flexible inflation targeting and potential output targeting.

.jpg)